The Signal the Market Is Sending

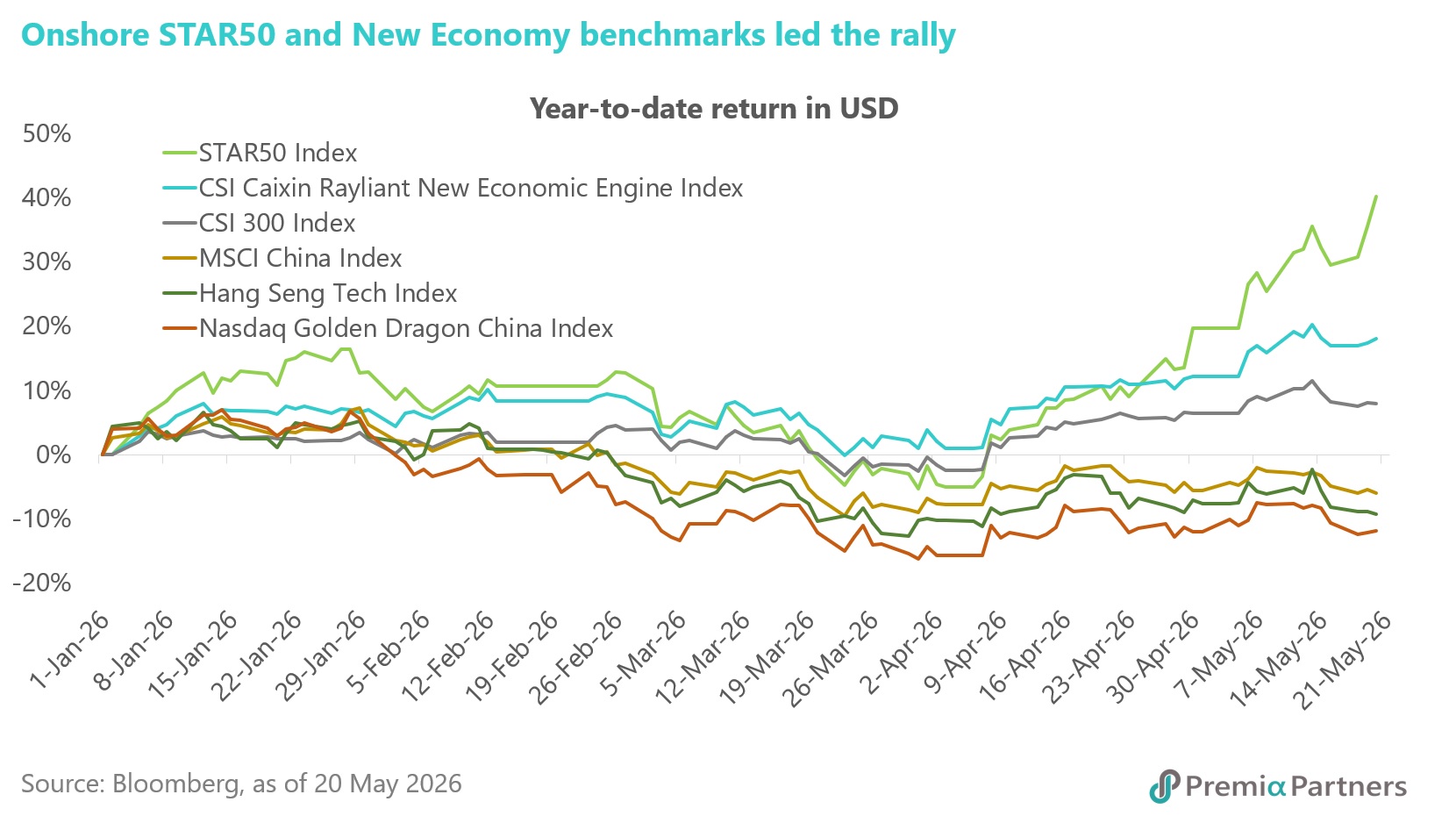

Not all rallies are created equal. As of May 20, 2026, the broad-based CSI 300 Index has posted a modest 7.6% gain year-to-date. Yet, that number obscures a more powerful and precise signal beneath the surface.

The STAR50 Index, focusing on the most strategically critical hard technology companies in China, has delivered a staggering 34.1% return over the same period. The CSI Caixin Rayliant New Economic Engine Index, capturing the broader tech and innovation ecosystem, is up 16.9%. Meanwhile, offshore benchmarks tracking Chinese equities have moved in the opposite direction: MSCI China is down 6.1%, the Hang Seng Tech Index has lost 13.2%, and the Nasdaq Golden Dragon China Index has fallen 9.8%.

This is not a marginal divergence. It is capital sending a strong signal, a decisive rotation away from legacy platform businesses and into the companies building, fabricating and exporting the foundational technologies of the next decade. Crucially, this rotation is earnings-driven rather than speculative. STAR50 earnings-per-share are forecast to grow 101.7% in 2026, more than four times the A-share broad market’s projected 21.9% growth. The valuations are justified by the earnings growth fundamentals, and increasingly vibrant STAR Market with strong set of policy-aligned hard tech sector leaders, and a robust IPO pipeline that covers a wide ranging set of strategic growth sectors from AI, new energy, new material, biotech innovators to also quantum and aerospace technologies.

For investors, the question is no longer whether to invest in China’s hard-tech transformation, but how to do so with precision and conviction. This insight examines developments on the ground, highlights key segments of the ecosystem and their leading companies, and concludes with the IPO pipeline that may further strengthen the structural investment case.

The Macro Engine: Reflation, Policy and the 15th Five-Year Plan

The structural backdrop for this rally begins at the macro level. China's producer prices have turned positive after more than three years of factory-gate deflation, leading to an inflection point for risk assets. Historical research shows that equity markets deliver their strongest returns when economic growth stabilizes alongside gently rising inflation, specifically when PPI runs in the 2–4% range. That window is open today.

The cyclical recovery is being reinforced by an unprecedented policy commitment. China’s 15th Five-Year Plan — spanning 141 pages — mentions artificial intelligence more than 50 times and explicitly targets “decisive breakthroughs in key core technologies.” The state has earmarked massive investment in quantum computing, 6G infrastructure, embodied AI and machine-brain interfaces. This is not aspirational language, but a procurement blueprint — one in which many of the likely beneficiaries already form core holdings of the Premia China STAR50 ETF and the Premia CSI Caixin China New Economy ETF.

US-China technological rivalry provides a further structural tailwind. Despite a recent Trump–Xi meeting that established a “tactical stabilization” in diplomatic ties, the technology decoupling remains intact. President Trump has acknowledged that China has not approved domestic purchases of Nvidia's advanced H200 chips, a signal of Beijing's unyielding resolve to build sovereign AI infrastructure. Every restriction tightens the coil of domestic demand. The following companies sit at the center of this structural shift.

I. Chip Designers: Creating Silicon Architecture That Powers China’s AI Infrastructure

Cambricon Technologies — China's Answer to Nvidia

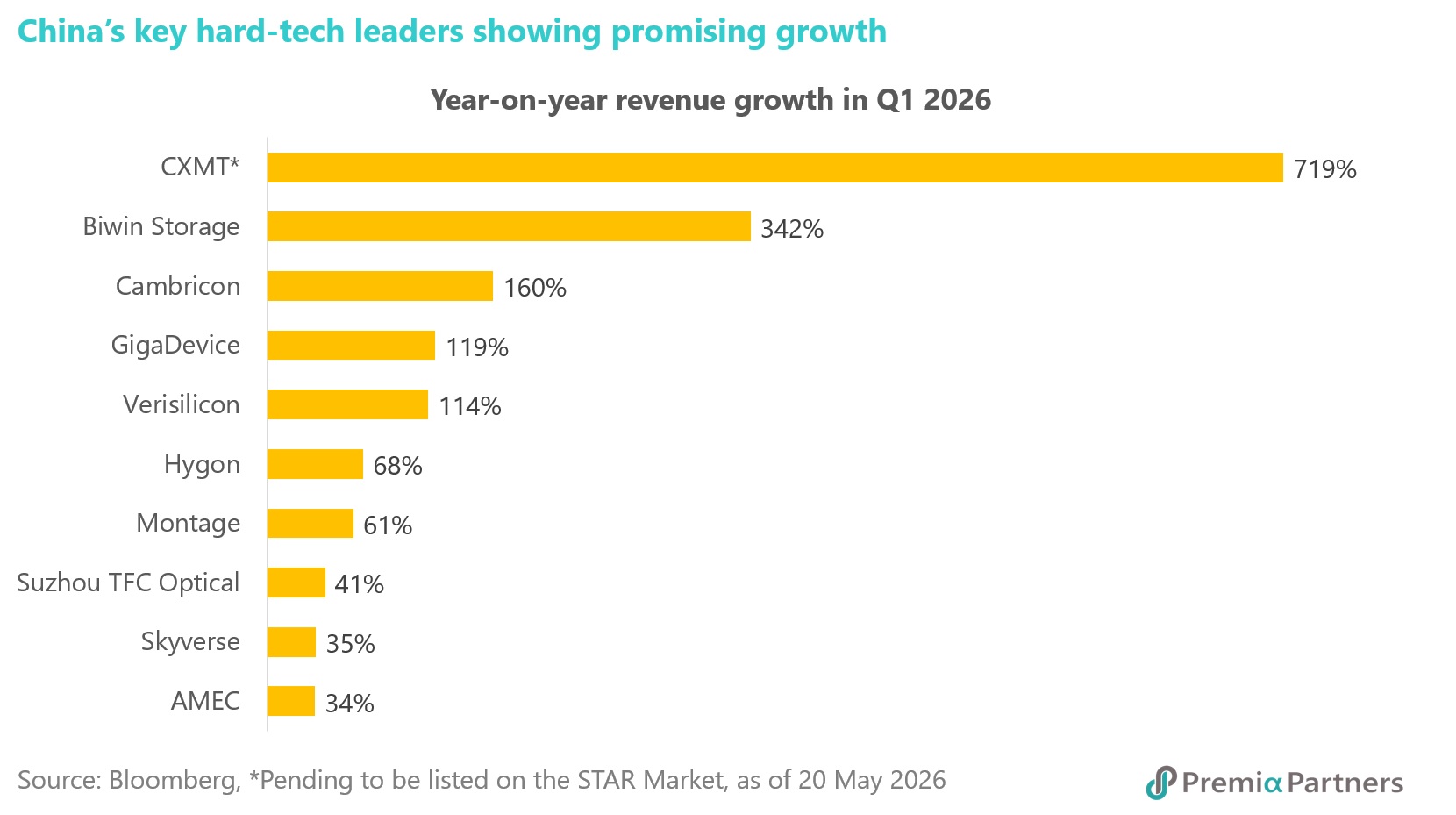

For a decade, Cambricon Technologies laboured in the shadow of Nvidia, burning cash as it built the architecture for a future that seemed perpetually around the corner. That future has arrived at an extraordinary speed. In Q1 2026, Cambricon reported revenue of RMB 2.89 billion, a 160% surge year-on-year, while net profit soared 185% to RMB 1.01 billion. This followed the company's landmark 2025 full year, in which it posted RMB 6.5 billion in revenue and recorded its first-ever annual profit, swinging from a RMB 452 million loss in 2024.

Cambricon is one of only two companies on Beijing's approved AI hardware procurement list, alongside Huawei. It is targeting 500,000 AI accelerator shipments in 2026, a more than a fourfold increase from approximately 116,000 units in 2025. What makes these numbers particularly meaningful is their source: Cambricon's growth is driven not by training-cluster capital expenditure, but by real-world inference deployment at the chip level — the commercial-scale adoption that separates durable revenue from AI hype. Operating cash flow turned sharply positive in Q1, confirming that the business has moved decisively beyond development into commercial momentum.

Hygon Information Technology — The CPU/GPU Dual Champion

If Cambricon owns the inference layer, Hygon Information Technology is seizing the compute infrastructure that underlies it. Hygon's 2025 revenues reached RMB 14.4 billion, a 57% year-on-year increase, as its high-end processors found their way into AI servers across China's public and private sectors. For Q1 2026, the company’s revenue jumped 68.1% to RMB 4.03 billion while net profit increased 35.8% to RMB 687 million.

Hygon is notable not merely for its growth rate, but for the breadth of its ambition. Its December 2025 “Dual-Chip Strategy” pairs Hygon CPUs with Hygon DCU accelerators into a fully integrated AI engineering platform, breaking the dependence on foreign CPU-GPU combinations that have historically constrained domestic AI infrastructure. Its proprietary High-Speed System Link (HSL) protocol, launched in September 2025, eliminates the communication bottleneck between CPUs and accelerators and fosters full-stack collaboration across AI chips, operating systems and OEMs. Hygon is not only substituting foreign components but also redefining the domestic AI compute stack.

Montage Technology — The Memory Interface Gatekeeper

Every AI server is packed with high-bandwidth memory, and every byte of that memory passes through a register clock driver or memory buffer that determines whether the system performs or crashes. Montage Technology has stormed into the global DDR5 top three — a remarkable achievement for a domestic Chinese chip designer competing against entrenched Western and Korean incumbents. As AI server buildout accelerates and DDR5 displaces DDR4 across the global fleet, Montage holds an obligatory chokepoint in the supply chain. Its products are non-negotiable components in every high-performance server deployed today, making it a quiet but powerful beneficiary of the global AI infrastructure wave. In Q1 2026, the company delivered a significant growth rate of 61.3% in net profit with an improved gross margin of 69.8%.

Verisilicon Microelectronics — The Silicon Intelligence Platform

Verisilicon occupies a unique position in the ecosystem as a platform IP provider and turnkey chipmaker across AI, automotive and consumer electronics. The company provides essential semiconductor intellectual property and end-to-end chip design services, the hidden layer enabling dozens of AI accelerator and SoC designs to reach production efficiently. As AI applications expand from data centers into edge computing, autonomous vehicles, and IoT, Verisilicon's platform model generates an ever-broadening revenue base without requiring the capital intensity of a traditional fab-dependent model. In Q1 2026, its operating revenue surged 114% year-on-year to RMB 835.7 million, while new orders rose to RMB 8.24 billion as of the end of April, with AI computing orders making up over 91%.

II. Fab Enablers: Turning Design Breakthroughs into Physical Silicon at Scale

Semiconductor Manufacturing International Corp. (SMIC) — The Foundry Backbone

Behind every Chinese chip design success story is a foundry that has to manufacture it at scale. SMIC is targeting a combined ramp of advanced 7nm-class wafer capacity from under 20,000 units currently to 100,000 units within one to two years — a five-fold expansion that would meaningfully close the manufacturing gap with global peers and provide the production backbone that Cambricon, Hygon and the next generation of domestic chip designers urgently need. It has also started R&D on 3nm wafters using Gate-All-Around surround gate technology and two-dimensional materials, with a tape-out expected this year. Additionally, 3nm carbon nanotube-based wafers have completed laboratory verification and are being adapted to the production line.

Advanced Micro-Fabrication Equipment (AMEC) — The Picks-and-Shovels Kingpin

If SMIC is the factory, AMEC supplies its tools. AMEC is the country's leading manufacturer of etch systems, the machines that carve nanometer-scale circuit patterns into silicon wafers. AMEC's tools are qualified at process nodes as advanced as 5nm, and its equipment is deployed not only across China but at leading chipmakers in Taiwan, South Korea, Japan and Europe. The company reported Q1 2026 revenue of RMB 2.92 billion and recurring net profit of RMB 478 million, up 34.1% and 60.0% year-on-year, respectively.

In the 2025 TechInsights Semiconductor Supplier Awards — the industry's most respected customer satisfaction survey — AMEC took first place in both “WFE to Foundation Chip Makers” and “Deposition Equipment” categories, beating Western and Japanese incumbents on quality and service. As every incremental fab capacity investment in China generates direct tool demand, AMEC sits at a uniquely privileged intersection: the full force of China's semiconductor capex cycle passes through its order book.

Skyverse Technology — China's Answer to KLA

If AMEC's etch machines carve the nanoscale patterns into silicon, Skyverse Technology's instruments verify that every cut is perfect. The company targets one of the most import-dependent niches in the entire semiconductor supply chain: quality control equipment. Its portfolio spans two core families — inspection systems, including the Redwood-900 series capable of detecting defects at the 10nm scale, and metrology tools that measure film thickness, layer flatness and lithography overlay accuracy down to sub-nanometer tolerances. Together, they are the eyes of the modern fab — the quality gatekeepers without which advanced chip manufacturing at scale is impossible.

Skyverse's strategic target is explicit: KLA Corporation, the American incumbent that has dominated global semiconductor quality control for decades. That dependency is ending. Skyverse's tools are already deployed at SMIC and YMTC — the very fabs racing to ramp China's advanced node capacity. In Q1 2026, revenue grew 34.6% year-on-year, with total assets expanding 77.9% as the company reinvests heavily in R&D to compete at the frontier. Every renminbi of domestic semiconductor capex generates a direct demand signal for Skyverse's order book.

III. Advanced Manufacturing and Networking: The Nervous System of AI

Suzhou TFC Optical Communication — The Global CPO Champion

While semiconductor investors focus on chip designers, Suzhou TFC Optical is quietly capturing the most strategically critical piece of the AI infrastructure puzzle: the optical interconnects that allow individual AI chips to function as a unified system. This is the Co-Packaged Optics (CPO) market, an emerging segment that Goldman Sachs projects will expand nine-fold to a USD 154 billion total addressable market as the industry migrates from 800G to 1.6T interconnect speeds.

TFC is more than a participant in this market; it is Nvidia’s development partner for next-generation CPO solutions now moving toward volume production. The company holds more than 200 patents in silicon photonics and 800G/1.6T optical technologies, while its R&D spending has risen nearly 60% in recent years, underscoring the scale of its technological commitment. In Q1 2026, revenue increased 41% year-on-year and net income rose 46%. As a key supplier to Nvidia, TFC benefits from both US hyperscaler capital spending and China’s domestic AI buildout, making it a rare dual-market export leader whose opportunity expands with each new GPU cluster deployed worldwide.

IV. Memory: The Supercycle Arrives and the Landmark IPO That Proves It

GigaDevice Semiconductor — The Fabless Memory Design Leader

GigaDevice Semiconductor is the quiet engine of China's memory self-reliance story. In 2025, the company reported record full-year results: revenue of RMB 9.2 billion, up 25% year-on-year, and net profit of RMB 1.65 billion, up 49.5%. The profit acceleration was even more pronounced in Q1 2026, with net profit surging 523% to RMB 234.6 million and revenue jumping 119% to RMB 4.19 billion. It is a clear signal of the memory upcycle gaining momentum.

The growth thesis is elegant: as Samsung and SK Hynix pivoted their advanced fab capacity toward high-bandwidth memory (HBM) for AI servers, a lucrative supply gap emerged in niche DRAM and SLC NAND Flash markets. GigaDevice, with its deep expertise in specialized memory products for industrial, automotive, and IoT applications, captured that gap with significant pricing power. Analysts describe GigaDevice as the convergence of three powerful tailwinds: AI demand, domestic substitution policy and the upward storage cycle.

Biwin Storage — The Supply Chain Beneficiary

Biwin Storage, China's leading provider of NAND flash storage modules and DRAM-based memory solutions, is a direct downstream beneficiary of the domestic memory manufacturing surge. In 2025, net profit surged 429% year-on-year to RMB 853 million as the memory upcycle rewarded its positioning across the enterprise storage and consumer memory value chain. In Q1 2026, the company reported an even stronger set of financials, with net profit reaching RMB 2.9 billion from a loss of RMB 198 million a year earlier and revenue surged 342%. Biwin's relationship with CXMT as a strategic investor and supply chain partner means its cost structure and supply security improve in lockstep with CXMT's production ramp, making it a leveraged play on the memory supercycle.

CXMT — The IPO That Could Shake the Global Semiconductor Order

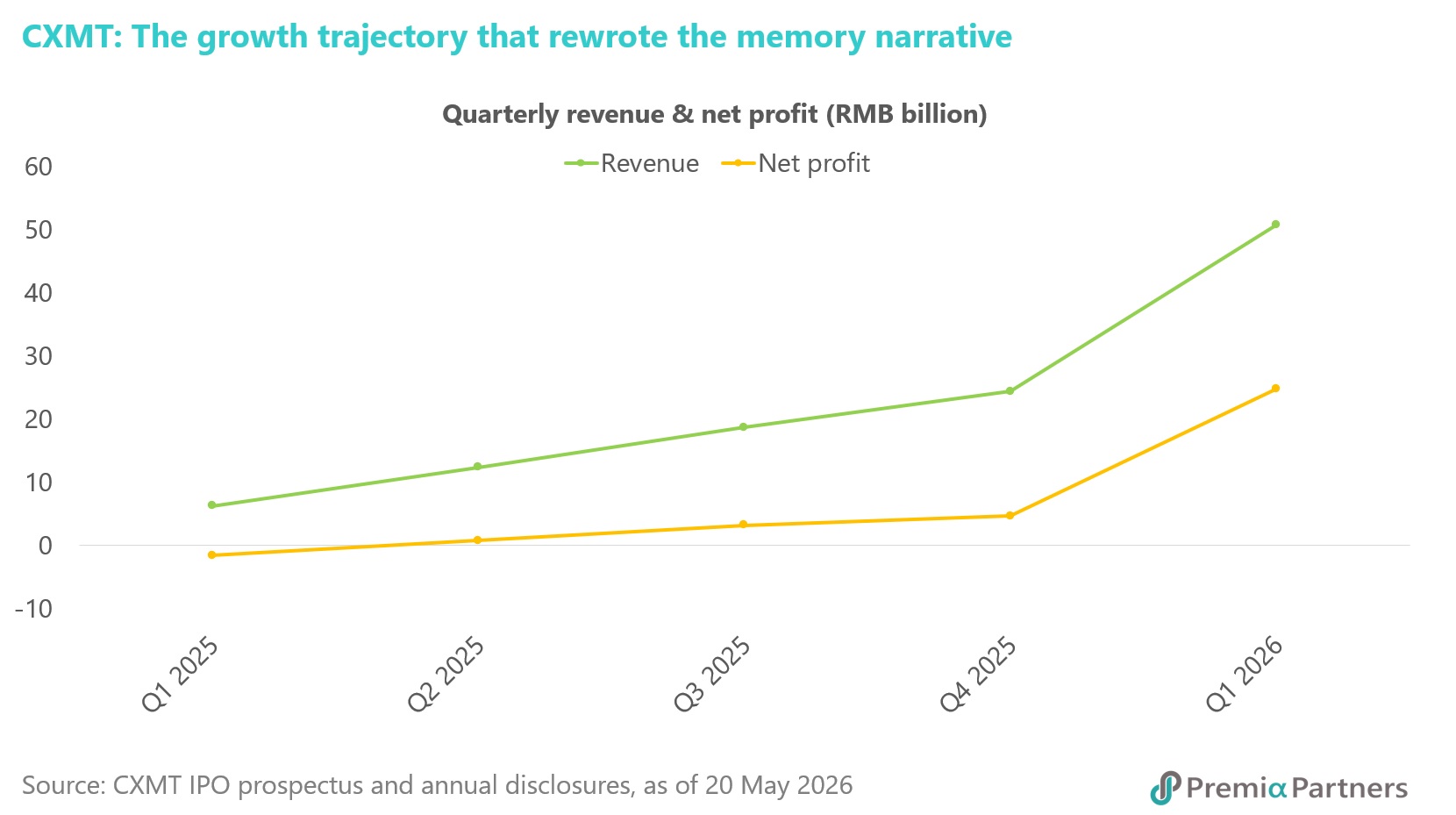

Among developments in Chinese semiconductors, few are as consequential as ChangXin Memory Technologies (CXMT), whose updated IPO prospectus sets out financial metrics of unusual scale and significance.

In Q1 2026, CXMT reported revenue of RMB 50.8 billion, a 719% year-on-year surge. Net profit attributable to shareholders reached RMB 24.8 billion, representing a 1,688% increase year-on-year from a net loss of RMB 1.6 billion in Q1 2025. Its guidance for first-half 2026 revenue stands at RMB 110–120 billion, with attributable net profit of RMB 50–57 billion, a sum that would entirely erase the RMB 36.7 billion in accumulated losses built up during its decade-long development phase.

The forces behind this explosion are structural. DRAM contract prices jumped over 75% year-on-year in Q4 2025 and rose by 98% in Q1 2026, as Samsung and SK Hynix diverted capacity toward HBM for AI, creating a significant supply gap in commodity DRAM. CXMT, which strategically stockpiled approximately RMB 28 billion of inventory during the price trough, was precisely positioned to capture the upswing. With a global DRAM market share now at approximately 7.67% and growing, CXMT has become a consequential participant in the memory market.

The company is seeking to list on the STAR Market and raise RMB 29.5 billion, which would make this one of the largest semiconductor listings in Chinese capital markets history. Institutional estimates, using a 20x multiple on projected 2026 attributable net profit of RMB 150–200 billion, suggest a potential market capitalization exceeding RMB 3 trillion — which would rank CXMT among the largest listed companies in China by market cap on day one. The ripple effects are already visible: CXMT's prospectus disclosures sent shares of GigaDevice, Biwin and other memory ecosystem names surging across the A-share market.

V. The IPO Pipeline: The Next Chapter Is Already Being Written

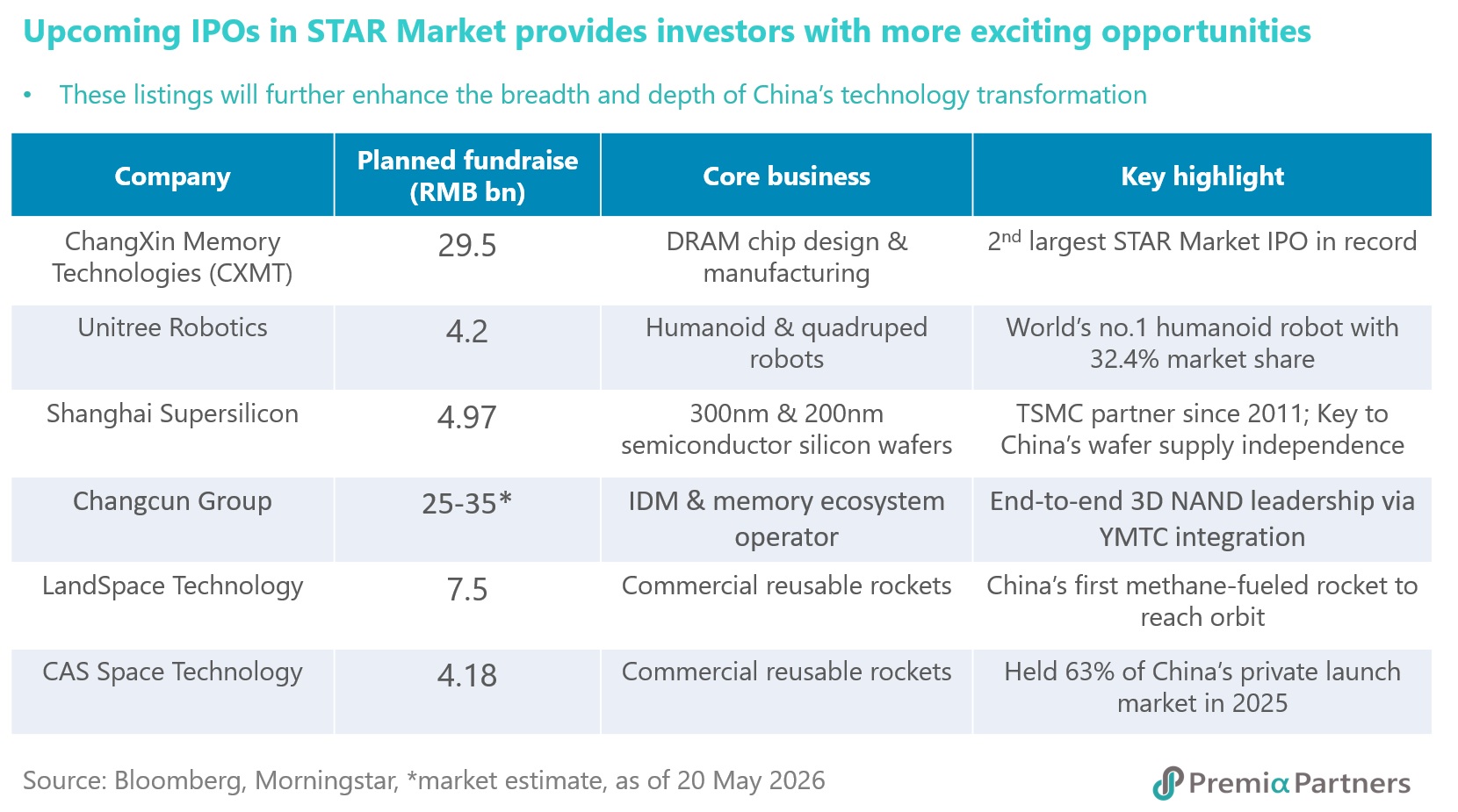

The CXMT listing is the headline, but it is not alone. Its fellow memory chipmaker Yangtze Memory Technologies Corp (YMTC) has also started the pre-listing tutoring phase with for STAR Market listing. The STAR Market's incoming IPO pipeline represents something broader: a generation of category-defining companies reaching the capital markets simultaneously, reinforcing the structural depth of China's hard-tech transformation.

Unitree Robotics – The most anticipated robotics listing in China's recent history filed a STAR Market IPO prospectus in March, seeking to raise RMB 4.2 billion. The disclosed financials are exceptional: 2025 revenue of RMB 1.708 billion, up 335% year-on-year, with gross margins of 60.3% and net profit of RMB 600 million after deducting non-recurring items. Unitree shipped more than 5,500 humanoid robots in 2025, capturing a 32.4% global market share — the highest of any manufacturer. In a pivotal strategic shift, humanoid robots overtook quadruped robots as the majority of revenue for the first time, reaching 51.5% of total sales. TrendForce projects Unitree and AgiBot will together account for approximately 80% of domestic humanoid robot shipments in 2026.

Shanghai Supersilicon – Shanghai Supersilicon is one of China's critical silicon wafer manufacturers, the substrate upon which every chip is built. Domestic wafer supply independence is a strategic prerequisite for true semiconductor sovereignty, and this listing, with an IPO size of RMB 4.97 billion, gives investors direct access to that structural demand.

Changcun Group – The company operates as an Integrated Device Manufacturer (IDM), controlling an all-in-one chip infrastructure that covers design, wafer fabrication, advanced packaging and testing. Yangtze Memory Technologies Co. (YMTC), China’s sole mass-producer of advanced 3D NAND flash memory chips, is the group’s crown jewel. Through its subsidiary Wuhan Xinxin, the group provides advanced wafer foundry services with a focus on NOR flash memory production and 3D hybrid bonding wafer integration.

LandSpace and CAS Space – China's commercial aerospace revolution is approaching the capital markets. LandSpace and CAS Space are competing to become the first commercial space companies listed on the A-share market — China’s “SpaceX moment.” Private capital is entering an industry that is rapidly transitioning from state monopoly to competitive innovation, with implications for satellite internet, precision navigation and commercial launch services that extend well beyond China's borders.

Taken together, these IPOs represent not merely investment opportunities, but data points confirming the breadth and depth of China's technology transformation. Each listing brings fresh, high-quality earnings growth into the STAR Market universe, continuously refreshing the investment opportunity set for funds like the Premia China STAR50 ETF and Premia CSI Caixin China New Economy ETF.

Two Vehicles, One Structural Conviction

For institutional investors seeking to capture this opportunity, the Premia ETF suite offers two precisely calibrated approaches.

Premia China STAR50 ETF (3151.HK / 83151.HK / 9151.HK) provides concentrated, high-conviction exposure to the upstream beneficiaries of China's chip sovereignty drive and AI infrastructure buildout. The STAR Market increasingly functions as China’s equivalent of a technology-focused growth board, and the STAR50 is its bellwether index. With a total expense ratio of 0.58% p.a., this ETF owns Cambricon, Hygon, AMEC, Montage Technologies, Verisilicon, Biwin Storage — the leading Chinese companies most directly leveraged to structural domestic demand for critical hardcore technology. The upcoming CXMT and Unitree Robotics listings are poised to enrich and deepen this universe further.

Premia CSI Caixin China New Economy ETF (3173.HK / 9173.HK) offers a broader, more balanced expression of the same thesis at a 0.50% p.a. expense ratio. It captures semiconductor manufacturers alongside the optically dominant networking plays like TFC, memory design champions like GigaDevice, the globally dominant CATL at the convergence of energy and AI infrastructure, and innovative companies generating high-margin revenue from global markets. For investors seeking exposure to China’s innovative economy with greater sector diversification, this ETF offers a more diversified approach to the country’s long-term technology and industrial transformation.