亚洲创新的投资机遇?

亚洲拥有世界60%的人口,为创新科技及消费市场带来具大的机会。随着该地区城市化发展、消费升级及人口老龄化等因素支持下,亚洲正在培育出独有的市场需求,且能更早的发展出创新机遇,并拥有庞大的市场潜力。另外,由于亚洲的监管环境及历史包袱相对少,使亚洲相对其他地区更具条件培育出创新企业,并在更快的时间达到规模效应。目前,亚洲已培育诸多出色的创新企业及独角兽,尤其以日本、中国、南韩和台湾为多。

在〈科技驱动创新:冲击重塑亚洲成长〉文章中,我们详细地阐述了亚洲创新发展的现况及行业影响,而本篇我们将针对PREMIA 亚洲创新科技ETF所涵盖的三大亚洲创新科技主题作大方向上的探讨,并介绍该策略的指数编制方法和特色:

1.数位转型

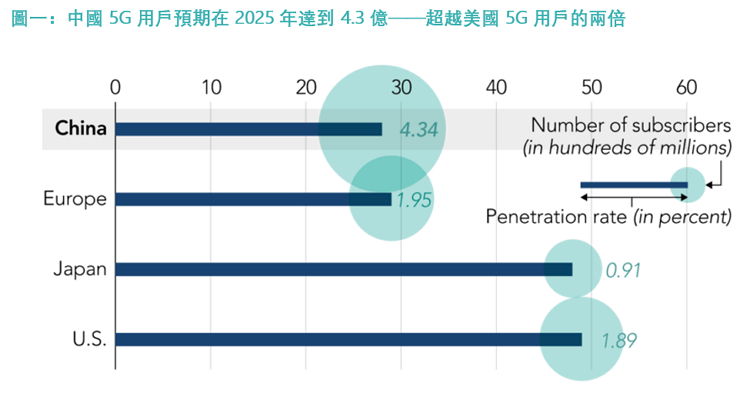

微软预期亚洲国内生产总值在2021年将有60%来自数位化产品及服务,数位转型正在重塑亚洲市场——亚洲具全球最高的数位化渗透率,其单独行动用户数量已达到28亿(该地区人口的67%);到2025年,行动用户数量预计将增加至31亿,占人口的72%。另外,亚洲行动网路商用计划在2018至2025年间将投入3,700亿美元建构新的5G网路。南韩今年已发布全球首个全国性的5G网路,预计到2025年,24个亚太市场都将推出5G,加速该地区数位转型及相关创新。据GSMA预测,中国将在2025年成为全球最大5G市场(图一),且5G将在未来15年为亚洲经济贡献近9,000亿美元。

数据来源:GSMA (2018)、Premia Partners

在〈亚洲 “数位革命” 如何改变我们的生活?〉文章中,我们深入探讨了亚洲数位革命下的三个技术相关领域;而在〈5G: taking off from the runway of growth〉文章中,我们在热门议题5G发展上有更详细的讨论。

2. 生物科技与医疗创新

亚洲65岁以上人口将在2030年占全球60%以上,这促使亚洲地区积极发展生物科技与医疗创新。并且,随着亚洲人均可支配收入逐渐提升,消费结构改变,医药商业模式从数量转为价值趋向,医疗数位化创新迅速发展,患者亦具备相关知识,近而增加医疗保健需求。亚洲预期在2022年成为全球最大的医疗物联网(Internet of Medical Things, IoMT)市场,将从目前的110亿美元成长至510亿美元,超越美国及欧洲市场(图二)。

3. 人工智能与机械自动化

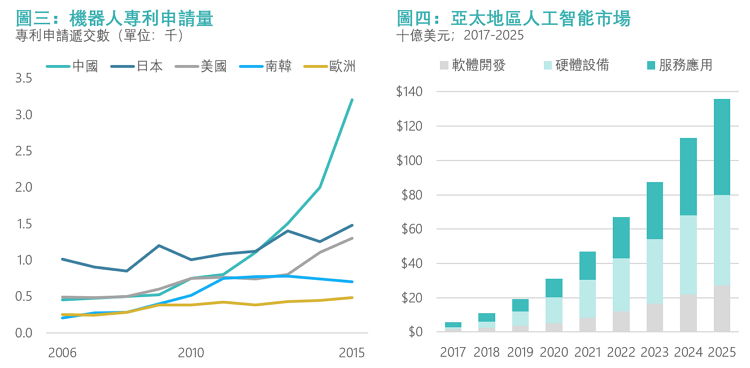

亚洲是世界工厂,但随着人口老龄化、教育程度提高及产业升级,该地区的劳动力成本逐渐升高,其在全球供应链的优势也逐渐消失。然而,这些国家地区化危机为转机,从低端的加工制造,迈向高端的技术创新,在国际上扮演推动机械自动化的重要角色——中国机器人技术研发在近五年翻倍成长,群冠全球,而日本和韩国亦维持国际领先地位(图三)。除了工业自动化的发展外,亚洲亦引领全球的人工智能创新,亚洲人工智能市场预期在2025年达到1,360亿美元(图四),中国将为领头羊贡献约70%,其后则为日本、南韩、印度及其他亚洲地区。

数据来源:金融时报、IDC、巴克莱研究、IFI、Tractica (2018年11月)、Premia Partners

在〈人工智能和机器人技术领域的领先企业〉文章中,我们以企业案例研究,阐述了更多关于此主题的发展。

精确捕捉亚洲创新科技大趋势:Premia FactSet 亚洲创新科技指数

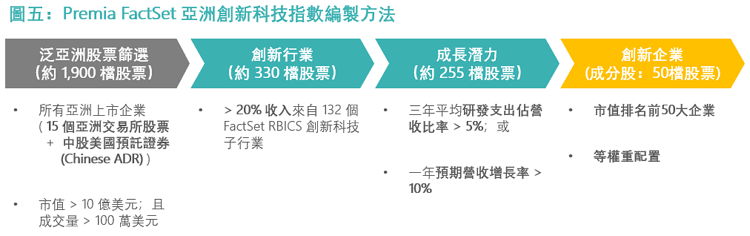

Premia FactSet 亚洲创新科技指数利用FactSet RBICS创新科技子行业分类系统,分析亚洲上市公司来自创新科技行业收入、公司整体成长潜力,以及对研发的持续投入等指标,评选在新兴科技和颠覆性技术行业领先的亚洲公司,最终筛选市值最大的50家企业,并以等权重配置指数,以避免过度集中风险及规模偏差。 Premia FactSet 亚洲创新科技指数系统化、精确地捕捉亚洲创新科技大趋势——数位转型、生物科技与医疗创新、人工智能与机械自动化,其编制主要有4个步骤(如图五):

数据来源:FactSet、Premia Partners

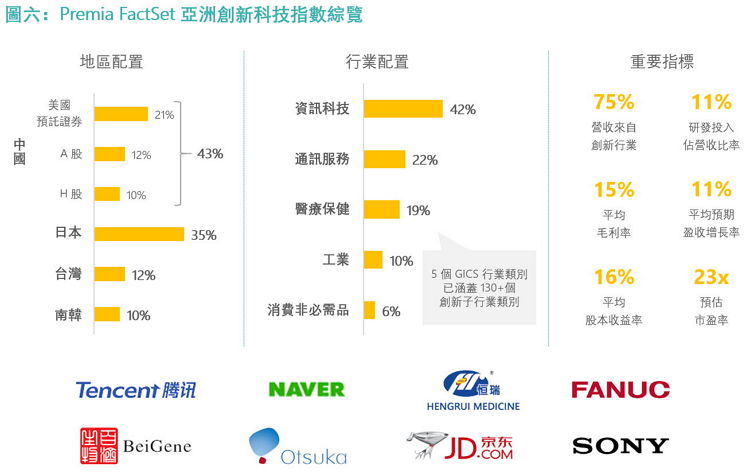

从上述指数编制方法可以看出,该设计同时考虑了企业创新科技的盈利能力及成长潜力,系统化地筛选出亚洲领先的创新科技企业。接着,我们可以从图六看到Premia FactSet 亚洲创新科技指数的配置、重要指标及持有的知名企业。该指数主要配置于北亚,以中国及日本为主——前者为引领全球数位革命及人工智能发展的重要大国,后者正推动全球自动化革命,且具备国际前瞻性医疗创新技术。就行业配置而言,资讯科技占比最高,其后的通讯服务、医疗保健、工业及消费非必需品亦皆为亚洲创新科技的成长动能。整体而言,Premia FactSet 亚洲创新科技指数有75%的营业收入来自我们所筛选的创新行业,且其研发、毛利率、预期营业收入增长率及股本收益率皆为水准之上,同时保持约20倍左右的市盈率。以增长型股票而言,该指数具备低成本持有高质量股票的特色。

数据来源:FactSet、彭博、Premia Partners;地区及行业配置截至2019年6月28日;重要指标根据2019年6月再调整数据

最后,我们以指数成分股及其配置权重(图六)来说明等权重指数的特色——创新成长动能的来源是多元的,不会因为企业市值较小而被稀释。若以传统市值加权指数配置,光是前四档(即阿里巴巴、腾讯、三星和台积电)就占了54%!然而,投资者大可以自己轻松买入这四档股票。另外,我们可以由右边市值较小的公司观察到,这些透过严格缜密方法筛选出来的创新科技企业,尽管对亚洲创新做出了贡献,确实常因市值较小而被投资者忽略。所以,Premia FactSet 亚洲创新科技指数以等权重配置成分股,避免过度集中风险及上述的规模偏差。

數據來源:彭博、Premia Partners;市值排名及最新權重截至2019年6月28日;等權配置根據2019年6月再調整數據

为什么要选择Premia 亚洲创新科技 ETF (3181 HK / 9181 HK)?

1. 透过单一产品捕捉亚洲创新大趋势: 数位转型、生物科技与医疗创新、人工智能与机械自动化

2. 聚焦于亚洲区内受创新技术支持的行业领导者: 与FactSet合作、基于其独有的RBICS公司细分行业收入系统进行筛选

3. 具成本效益:经常性开支仅每年0.50%