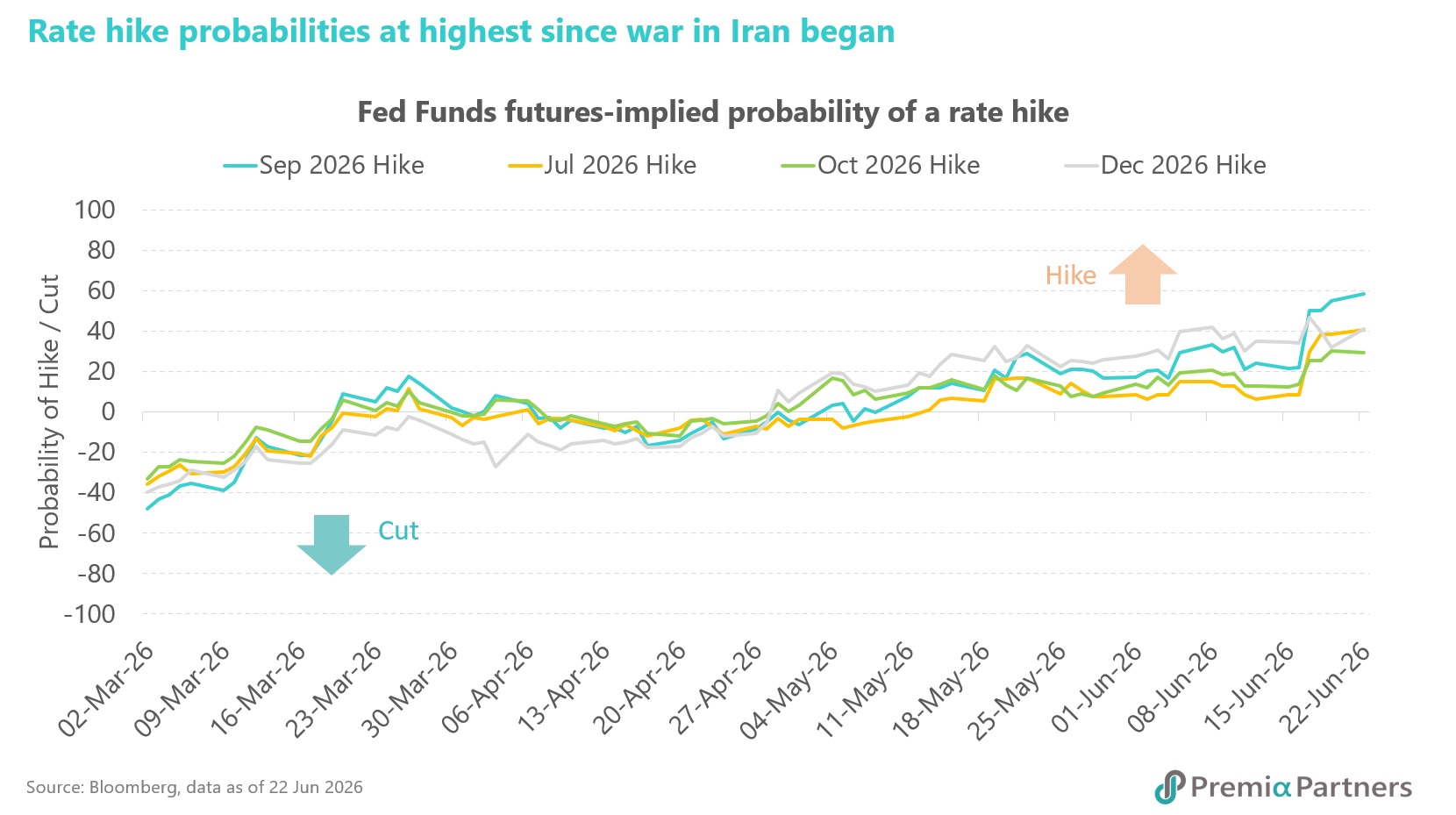

New US Federal Reserve Chair Kevin Warsh’s first FOMC held rates at 3.50–3.75%, but the tone skewed hawkish. He skipped submitting a dot, while Fed rates projections shifted higher, with the 2026 median rising to 3.8% from 3.4%. Markets reacted accordingly: 2-year yields rose, equities fell, and the dollar strengthened. The bond market has also started to re-priced aggressively over the week. Market is now forecasting rate hikes as early as September 2026.

Why the yield won’t roll over easily

The inflation data tells a structurally sticky story — one that makes it genuinely difficult to bring the front end of the rate curve down quickly.

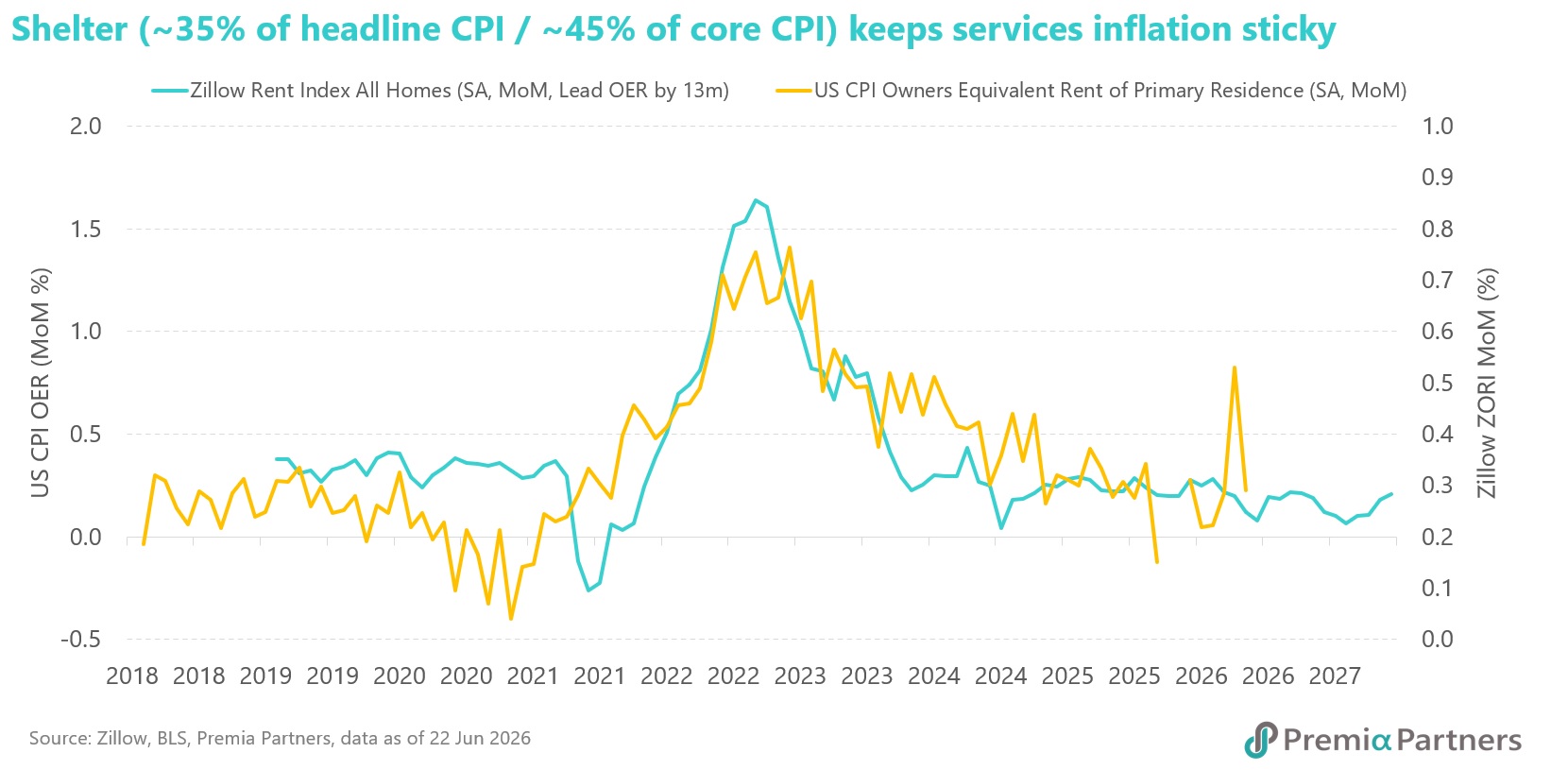

Services inflation is slow to unwind. Services account for roughly 68% of the CPI basket, with shelter alone approaching 40%. Both adjust with a lag — shelter through lease rollovers, services through wages — meaning progress depends on rent and labour markets easing in tandem. Goods prices are more responsive but carry less weight (~32%), limiting how much they can offset the stickiness elsewhere.

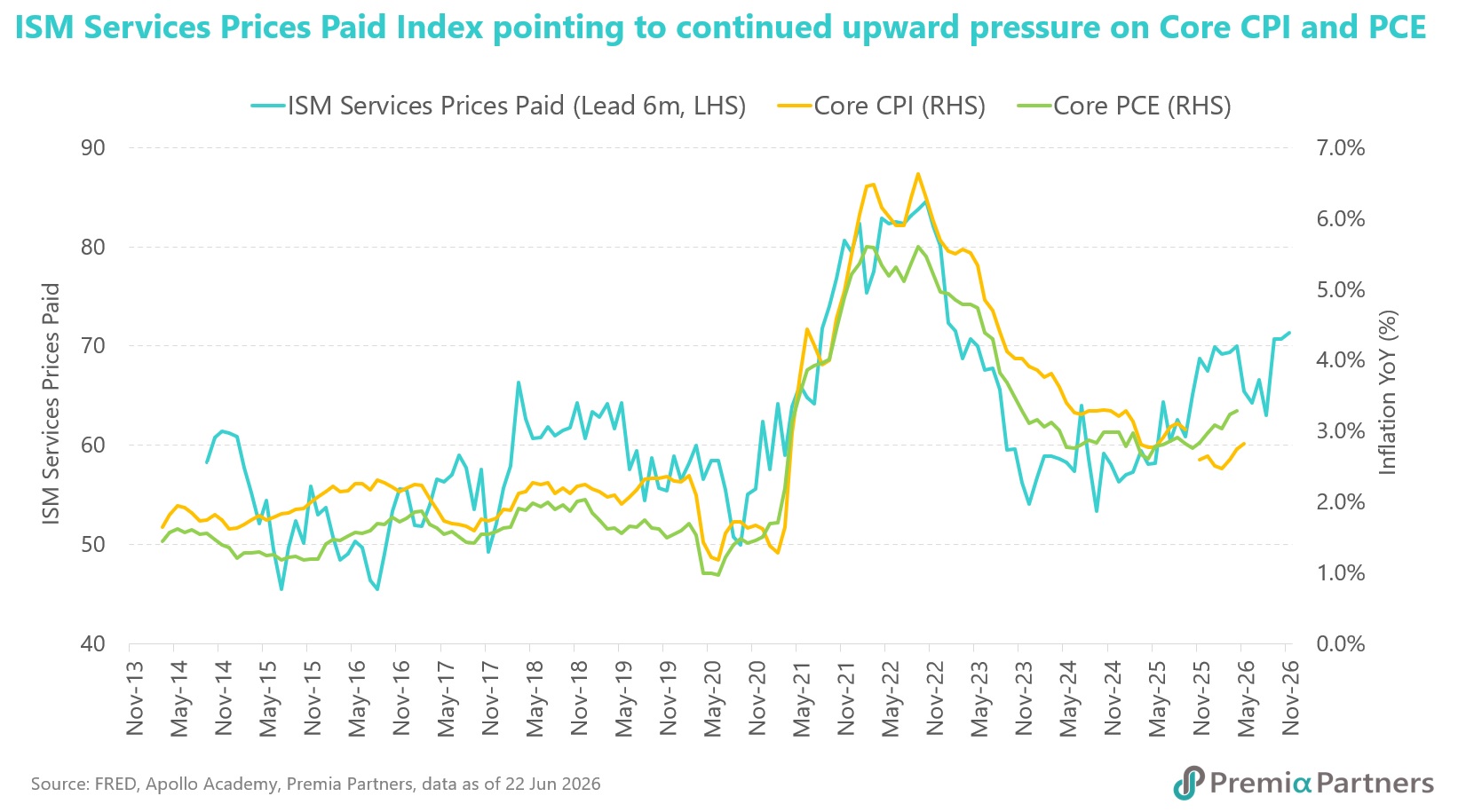

The pricing pipeline shows inflation pressure are building. The indicators that typically lead inflation— PPI (factory gate costs), ISM prices paid (large-firm input costs), NFIB (pricing intention for small business) — have been running well above their historical averages. ISM services prices paid, in particular, is at its highest reading since 2022. That matters because this series has historically led Core CPI and Core PCE by approximately 6 months. What the pipeline is signalling right now is continued near-term price pressure - not a fast cooldown.

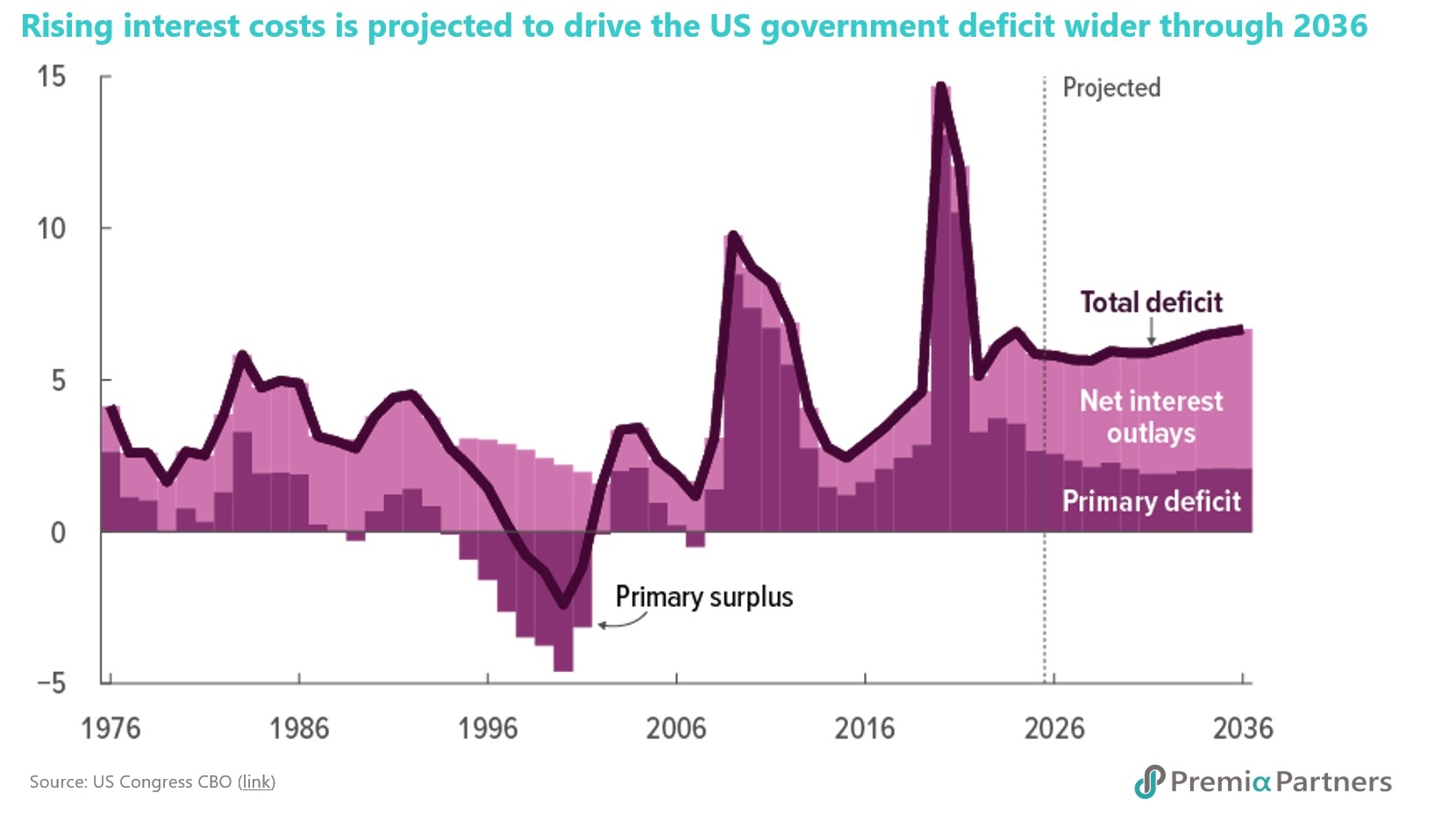

Structurally, US yield struggle to come down as government fiscal deficit is still growing – this means the US governments needs to keep issuance at a high pace to fund the fiscal budget, which creates upward pressure in treasury yield.

What does it all mean?

This may mark the start of a US rate hike cycle, and for investors holding conventional Treasuries or long-duration fixed income, the setup looks increasingly uncomfortable.

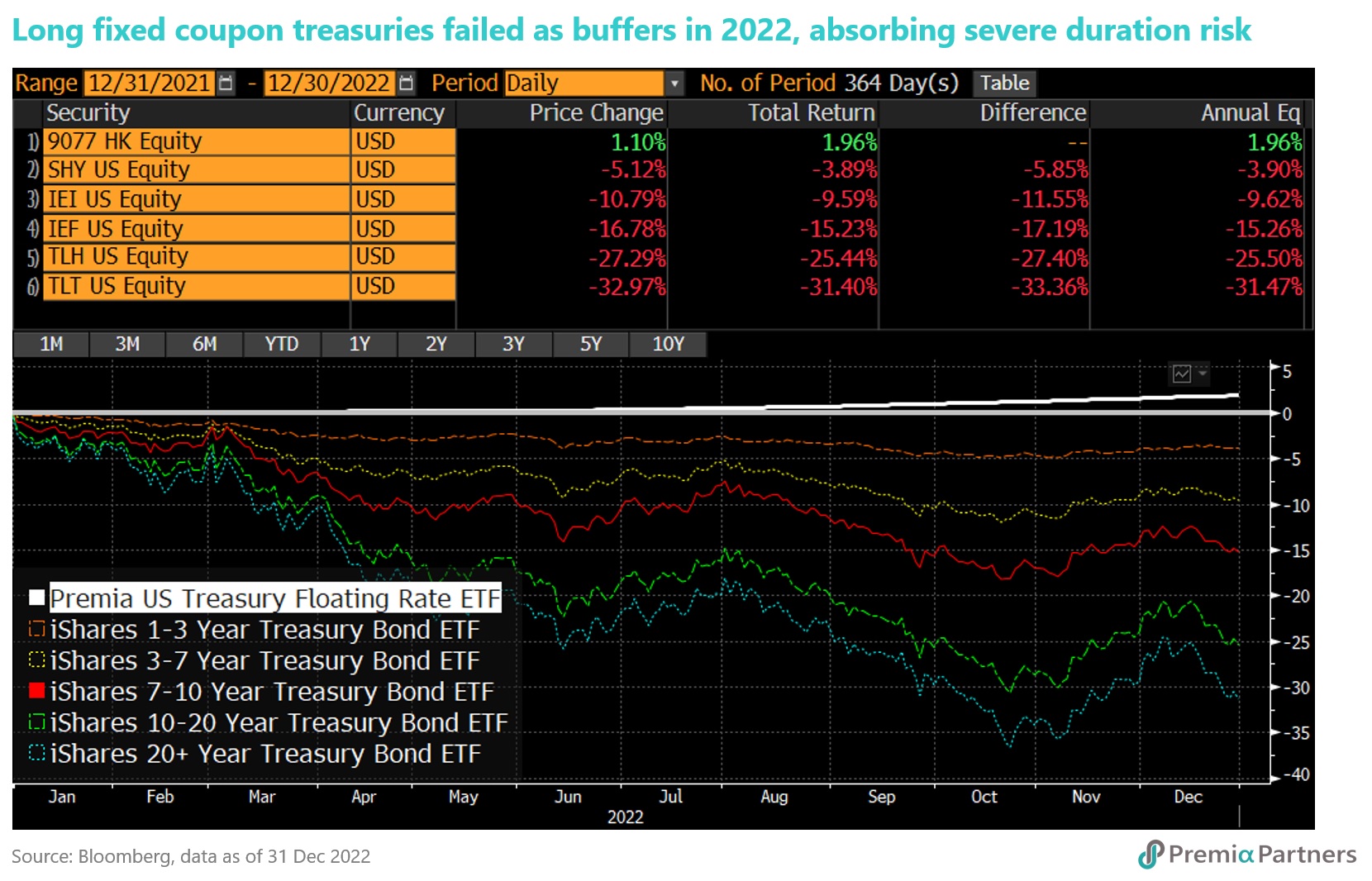

During 2022, the Fed hiked an unprecedented seven times, lifting the target range from near zero to 4.25–4.50% by year-end. Over that period, as the S&P 500 fell roughly 18%, long-duration US Treasuries dropped as much as 31% in a single year—failing to serve their traditional role as a buffer protecting investor capital. While this could be on the extreme end of the example, it serves to demonstrates long duration US Treasuries remain highly exposed to repricing at the long end, absorbing the bulk of duration risk.

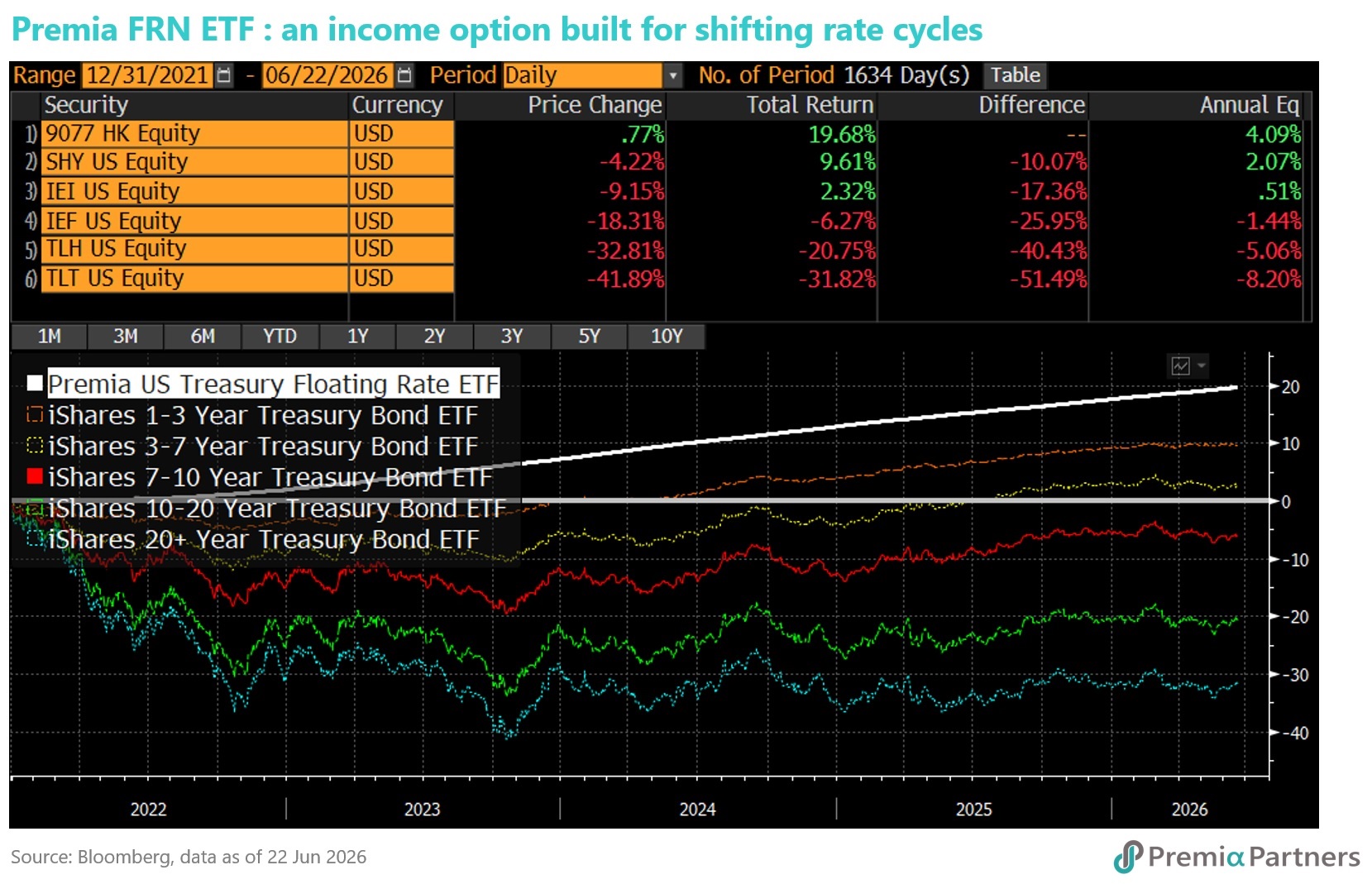

Where the Coupon Adjusts, So the Risk Doesn't Accumulate

Front-end rates may stay higher at least for the near future - and the Premia US Treasury Floating Rate ETF (3077 / 9077 / 9078 HK) is structured to get paid while they do.

The ETF holds US Treasury Floating Rate Notes (FRNs), part of one of the largest and most liquid bond markets in the world, with over US$670bn outstanding. Its coupon resets weekly to the 13-week T-bill rate, anchoring it directly to the front-end policy rate that the Fed has left elevated and the dot plot has biased higher.

That mechanism makes the outcome straightforward in either direction:

- If the Fed hikes, the coupon adjusts upward within days.

- If it holds, investors continue collecting current running yield of (~3.6% as of 22 June 2026) annualised.

Because the coupon floats, duration—sensitivity to changes in yield—is, for practical purposes, near zero.

With the terminal rate uncertain, the dot skew to the upside, and duration carrying asymmetric downside risk, harvesting an elevated, weekly-resetting front-end coupon—without the exposure fixed-rate bonds carry—can be a sensible positioning choice.