The geopolitical risks that dominated global markets for much of 2019 faded in the last quarter as the US and China reaching a phase one trade deal (which happened on Jan 15th and we discussed in China: Beyond Trade Deal Phase 1). As a result, global equity markets posted gains and China A shares also performed strongly in Q4 2019 against this backdrop.

FACTOR PERFORMANCE

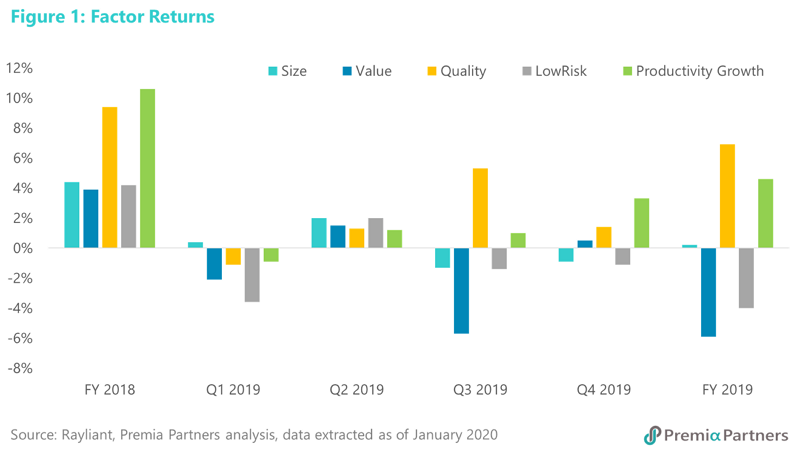

Productivity Growth was the best performing factor in Q4, followed by Quality. The two factors were the best performing factors in 2018 and they kept the trend in 2019. Value showed a slight sign of reversion in Q4 but remained the worst performing factor throughout the year.

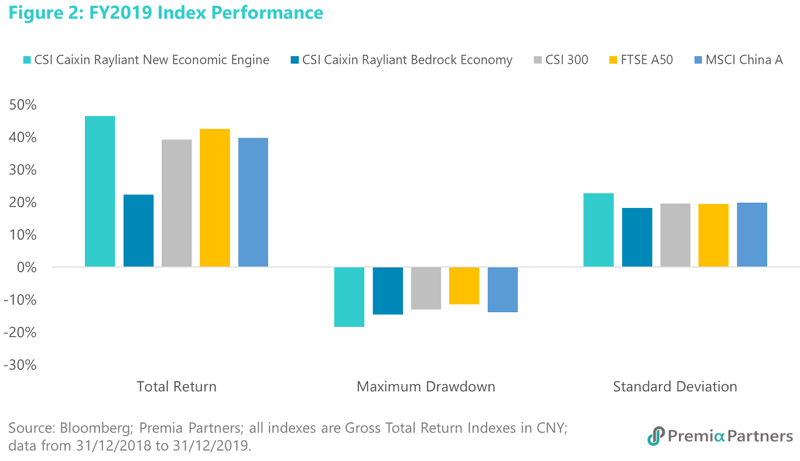

As a result, the two Premia multi-factor China A shares ETF saw different performances in 2019. Premia CSI Caixin China Bedrock Economy ETF, which is a defensive play with active Value and LowRisk exposures by design, trailed the broad CSI 300 market performance. On the other hand, Premia CSI Caixin China New Economy ETF, a quality growth play designed to capture high quality, high productive growth new economy companies, was among the top performing broad market China equity ETFs listed outside of China in the full year of 2019 with 43% total return in CNY terms (41% total return in USD).

What is Quality & Productivity Growth? - To recap, the factor definitions employed in the Premia multi-factor China A shares indexes, designed by Dr. Jason Hsu’s team at Rayliant Global Advisors are as follows –

· Balance Sheet Health (aka Quality in our usual definition): Debt Coverage Ratio, Cash Ratio, Net Profit Margin, negative Accruals, negative Net Operating Assets

· Productivity Growth: Gross profitability, Operating Profitability, negative Change in Total Assets, negative Change in Total Book Assets, R&D expense over Assets

Both of the two factors entail component metrics that are broadly considered as “Quality”, despite the fact that this late popular factor does not really have a commonly agreed definition compared to the widely accepted original Fama-French Size and Value. Dr. Jason Hsu recently published a paper titled “What is Quality”. The paper published in the Financial Analysts Journal won the 2019 Graham and Dodd Top Award, and for those interested can find it on SSRN.

2019 was firstly a year of recovery from 2018, but also a year of P/E multiple expansion across industries. New economy sectors, in particular, had a strong year as the government continue to drive policies around its reconfiguration toward a service-oriented, consumption-led, technology first economy despite the headwinds from the US-China trade dispute, or even to a greater extent with the conflict as an alarming catalyst.

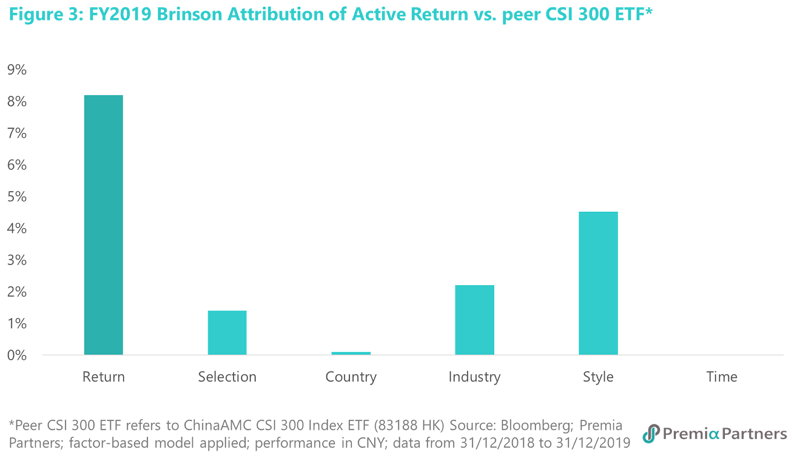

Our Premia CSI Caixin China New Economy ETF (3173/9173 HK) saw active return not only in the style factors but also from such new economy industry allocation and selection compared to peer ETFs tracking the broad CSI 300 index, as shown in Figure 3.

2020: VALUE MIGHT REVERT, BUT QUALITY (NEW ECONOMY) GROWTH WILL CONTINUE TO SHINE

Heading into 2020, we believe the price multiple expansion would continue but at a slower speed and be more selective on sectors, especially as China further develops into a two-speed economy. From an industry perspective, new economy sectors such as technology services, advanced manufacturing, new energy and healthcare will continue to be the megatrend growth opportunities and key drivers of China’s overall economic and productivity growth in the long term. On the other hand, as earnings play a bigger role in the P/E * EPS formula for market value, sector leaders with solid profitability and earnings capabilities stand better chances to outperform. From a style factor perspective, the broad set of Quality factors are best positioned to continue generating positive risk premia. The quality growth play would remain ideal for investors looking for megatrend growth opportunities in A-shares, while allocators more concerned about potential downside risk or wish to take a contrarian approach may consider the value strategy.

Further readings

China: Beyond Trade Deal Phase 1

Insights from the revenue forecast in China market

China A Factor Review: 2019 Q3